What's New?

January 2025

Tax Season is Almost Here

Your year-end statements had a list of mailing dates for tax information, but we wanted to highlight the details for you:

- Jan. 17th: 1099s for education and retirement accounts will be mailed

- Jan 17th – Mar 7th: 1099s for non-retirement accounts will be mailed. The timing of your 1099 will depend on the type of investments in your account. Mutual funds, REITs, UITs, international investments and municipal bonds typically have more complicated reporting and it takes a little while longer for the issuers to forward the information to LPL

- Feb 21st & May 23rd: 5498s will be mailed. Form 5498 details any contributions, transfers or rollovers to and between retirement accounts. This form is not required to file your taxes, so please don’t panic if you receive yours in May. Just keep it with your tax documents. If you’re ever audited and the IRS questions where your retirement plan went, this form will be your paper trail

All of the tax forms are posted on your LPL website as soon as they’re available. If you have not signed up for web access through Account View yet, please contact us or go to https://accountview.lpl.com/web/login to register.

Social Security Fairness Act

For anyone working (or recently retired) in the public sector, there was an important piece of legislation enacted this past weekend. The Social Security Fairness Act was signed into law on Sunday. The new law could impact social security benefits for you and your spouse. If you are a police officer, firefighter, nurse, postal worker, public school teacher or government employee with a pension, you are probably familiar with the Windfall Elimination Provision (WEP) and Government Pension Offset (GPO). These provisions reduced social security benefits for some retirees that received pension income. It also reduced or in some cases, eliminated survivor benefits to spouses. Retroactive to Jan 1, 2024, these two provisions no longer exist. Some of you may see a lump sum payment for 2024 applied to your benefits and you also may see an increase in your monthly social security payments moving forward. The logistics of the lump sum payment have not been detailed yet, but there is nothing you would need to apply for or file for to receive the payments. There are almost 3 million public sector employees who will be impacted by this change, so it’s a big deal! If you are affected by this change, please make sure to update us so we can adjust your income projections and estate plan.

December 2024

10 years and counting!

Calderon Fortney Financial Group is once again proud to announce that Matt has been recognized by Connecticut Magazine as a 5 Star Wealth Manager. This is Matt's 10th time receiving this recognition!

Calderon Fortney Financial Group is once again proud to announce that Matt has been recognized by Connecticut Magazine as a 5 Star Wealth Manager. This is Matt's 10th time receiving this recognition!

Wealth managers are nominated by clients and peers and do not pay a fee to be considered or included on the list. While no one should work with a financial planner based solely on a listing in a magazine, it does reinforce the good work we do and the reputation we have.*

*Award based on 10 objective criteria associated with providing quality services to clients such as credentials, experience, and assets under management among other factors. Wealth managers do not pay a fee to be considered or placed on the final list of 2014, 2015, 2017, 2018, 2019, 2020, 2021, 2022, 2023 or 2024 Five Star Wealth Managers

More Insurance Education with MoneyGeek

We've  provided more expert commentary to MoneyGeek on life insurance. This month, Matt shares his thoughts on some insurance basics and whether $500k of life insurance is an appropriate amount of coverage. Check it out HERE.

provided more expert commentary to MoneyGeek on life insurance. This month, Matt shares his thoughts on some insurance basics and whether $500k of life insurance is an appropriate amount of coverage. Check it out HERE.

You can also head over to our Moneygeek.com Contributions page and see our entire library of collaborations!

Last minute ways to reduce your taxable income in 2024

Are you looking to manage your tax liability before the end of the year? Are you looking to help a qualified charitable organization? You can do both at the same time, if you do it correctly!

- Generally speaking, contributions to charitable organizations may be deducted by up to 50 percent of your adjusted gross income

- Got stock gains? Appreciated stock can be gifted to a charity. You get a deduction for the fair market value and the charity can make a tax exempt sale

- Not sure what to do with your Required Minimum Distribution (RMD)? You can have up to $105k of your RMD sent direct to a charity. You avoid having it count as taxable income and the charity gets a nice gift

- Looking to help out a child or grandchild instead? Depending on the state you file taxes in, contributions to a 529 plan may be state tax deductible. Some states even allow deductions for contributions to out of state plans or plans owned by someone else.

Talk to one of our financial professionals for more information and strategies to help manage your end of year tax planning*. Have a great Holiday Season!

*This information is not intended to be a substitute for specific individualized tax advice. We suggest that you discuss your specific tax issues with a qualified tax advisor.

November 2024

It's been a strong 2 years for the stock market, particularly if you own some of the high flying tech stocks. We've seen significant appreciation in client portfolios, but along with those big gains could come a sizeable tax bill if you're selling appreciated positions in non-retirement accounts. Make sure you're monitoring your potential capital gains tax and use these last 2 months to try and offset your gains with any capital losses. We've got a quick article on the what and how of capital gains taxation HERE. Your potential taxation will depend on your reportable income for the year, so reach out to your financial planner and CPA to see what your liability may be and ways you can work to minimize it.

September 2024

Blink and it will be the end of the year! There are numerous year end planning items to be aware of and we encourage you not to wait until the last minute to address them:

- Medicare enrollmen

t opens October 15th and runs through December 7th

t opens October 15th and runs through December 7th - FAFSA foms for the 2025-26 school year will be available by December 1st

- Increases to 401k contributions usually take 1-2 pay cycles to adjust and should be processed now

- Thinking about starting a 401k plan for your business? Get it set up now so you can make contributions before year end

- If you have Required Minimum Distributions from your retirement plans, they must be taken before December 31st

There could be many other items on your financial checklist and we encourage you to call or schedule an appointment to review what smart decisions you could be making with your money before the end of the year!

August 2024

We've got more to discuss with Moneygeek.com. Check out our dedicated page HERE for our latest thoughts on insurance and whole life companies.

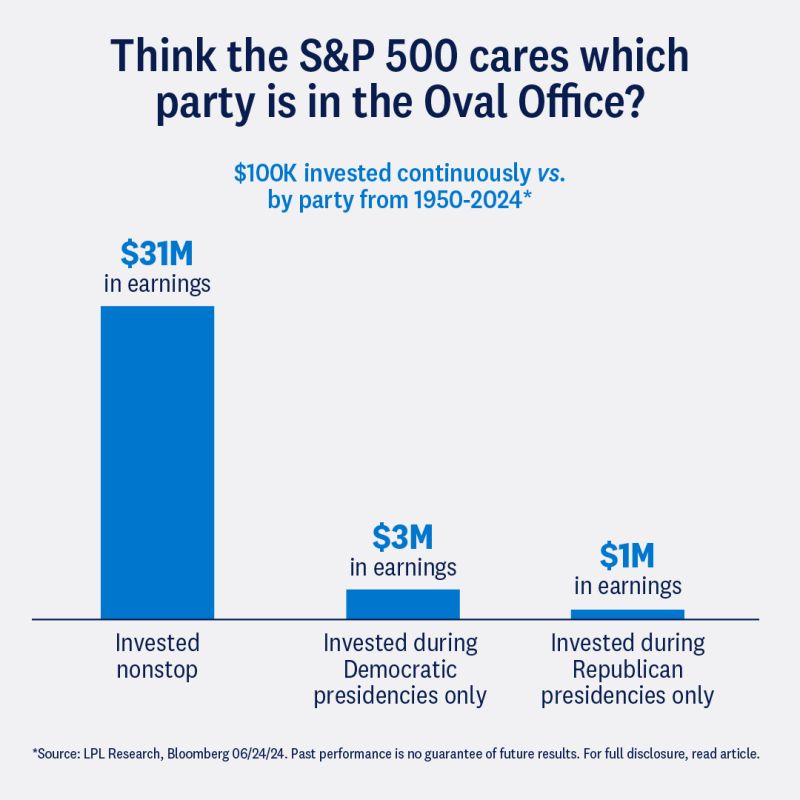

We're entering a contentious and  highly charged election season. With emotions running high, it can be very tempting to let your political opinions impact your investment decisions. We encourage you to keep politics out of your portfolio and focus instead on your financial plan and long term goals. Leave the market prognostications to cable news and maintain your discipline!

highly charged election season. With emotions running high, it can be very tempting to let your political opinions impact your investment decisions. We encourage you to keep politics out of your portfolio and focus instead on your financial plan and long term goals. Leave the market prognostications to cable news and maintain your discipline!

June 2024

We've collaborated again with Moneygeek.com on important questions regarding life insurance.

Ever wonder how the amount and cost you are offered for a policy is calculated? There are a number of factors that go into the equation and they may differ from company to company.

Ever discussed or read about using life insurance to save for retirement instead of a 401(k) plan? We continue to emphasize life insurance's primary goal is to leave money for your heirs. A 401(k)'s primary goal is to help you save for retirement. There are specific circumstances where individuals may need to look at alternatives, but only after a thorough review with a professional.

Navigate over to our Resources tab to find all our Moneygeek articles on insurance, as well as other important financial topics. Or you can click HERE!

May 2024

The school year is almost over and it's time to prepare for final exams and graduations. Are you researching how to help your child prepare for the cost of a secondary education? The first step is to start early! The longer you have to prepare, the greater the likelihood you'll be able to save and take advantage of compounding interest. How can you save? Consider some of the following ttax advantaged options:

- 529 College Savings Accounts- Your contributions grow tax deferred and can be withdrawn tax free if used for qualified education expenses. Qualified expenses include the costs associated with attending accredited high schools, trade schools and 2 or 4 year colleges

- Coverdell or Education IRAs- Your contributions grow tax deferred and distributions can be made tax free if used for qualified education expenses. There are annual income restrictions for opening an account and the funds must be used by the time the student is 30.

- Series EE or I Savings Bonds- Interest is typically state tax exempt and could be federally exempt if used for higher education. Be aware there are limits on age, income and who can claim the tax exemption.

There are other investment vehicles and ways to save for your child's education as well. Contact our office if you'd like to learn more about which option may be most appropriate for you.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results.

This information is not intended to be a substitute for specific individualized tax advice. We suggest that you discuss your specific tax issues with a qualified tax advisor.

April 2024

As you finish up your 2 023 tax returns and strategize with your financial planner and CPA about ways to reduce your tax liability, make sure you're aware of the following options and scenarios:

023 tax returns and strategize with your financial planner and CPA about ways to reduce your tax liability, make sure you're aware of the following options and scenarios:

- Roth IRAs are great, but..... make sure you understand you'll owe income tax on any amount you convert from a Traditional IRA or 401k. You'll need to have cash on hand to cover your tax liability. Also, be aware of how that added income could affect social services such as your social security benefits or Medicare premiums.

- Qualified Charitable Distribution- Are you receiving a Required Minimum Distribution (RMD), but don't really need it? You can have up to $100k of your RMD donated direct to a charity. You won't be required to report the RMD as income or be taxed on it.

- Are you using your state's 529 College Savings Plan for your kids?- Many states offer a state tax deduction to residents for contributing to their sponsored 529 plan. It's not a huge deduction, but it could make a difference!

- Check your withholding at work- One of the most common tax mistakes we see are clients not having the appropriate withholding amounts on their paychecks. If you've changed jobs, received a raise, got married/divorced, had kids or can't claim your kids anymore, make sure you're double checking how much is being withheld from your paycheck. It could cost or save you thousands of dollars.

March 2024

Don't let the sun s et on your estate plan. The Tax Cuts and Jobs Act of 2017 (TCJA) raised the estate tax exemption to approximately $13.1 mil this year. That's a significant number that many people won't need to be worried about. But the exemption is set to sunset and revert back to pre-TCJA levels at the end of 2025. The limit will then likely drop to around $7 mil. That's a number we know will affect a much greater number of individuals. You can either hope Congress will enact new legislation, or you can talk to your financial planner and estate attorney about ways to shelter your estate from additional taxation. Don't get caught scrambling to find a lawyer after Thanksgiving of 2025. Start having the discussions with your wealth management team now!

et on your estate plan. The Tax Cuts and Jobs Act of 2017 (TCJA) raised the estate tax exemption to approximately $13.1 mil this year. That's a significant number that many people won't need to be worried about. But the exemption is set to sunset and revert back to pre-TCJA levels at the end of 2025. The limit will then likely drop to around $7 mil. That's a number we know will affect a much greater number of individuals. You can either hope Congress will enact new legislation, or you can talk to your financial planner and estate attorney about ways to shelter your estate from additional taxation. Don't get caught scrambling to find a lawyer after Thanksgiving of 2025. Start having the discussions with your wealth management team now!

January 2024

Tax forms will be mailed every Friday, beginning Jan. 19th. Retirement account forms will be received the earliest. Investment accounts will be staggered throughout February and into early March, depending on the type of investments you own. Accoounts with real estate, municipal bond or international holdings tend to take longer for reporting. All statements are posted on AccountView as soon as they're available. Head over to our Client Account Web Links page to get yourself enrolled!

We've partnered with Moneygeek.com again to offer some insights on Life Insurance as an investment vehicle. We've also shared our thoughts on the difficulties some people have in saving for retirement. Check them out!